The change in sentiment surrounding Wall Street has been palpable as stubborn inflation continues in its refusal to subside.

Following December’s buoyant outlook and the expectation among some that rate cuts could come as soon as March, markets are now having to react to the very real possibility that there may be no cuts at all this year. But how could a higher-for-longer scenario impact the S&P 500?

March had been pinpointed as an optimistic stage for the beginning of the Fed’s switch to a dovish monetary policy as the battle against inflation continued to be won. Instead, it was March’s Consumer Price Index (CPI) figures that sparked concern throughout Wall Street.

CPI inflation surpassed expectations to post a

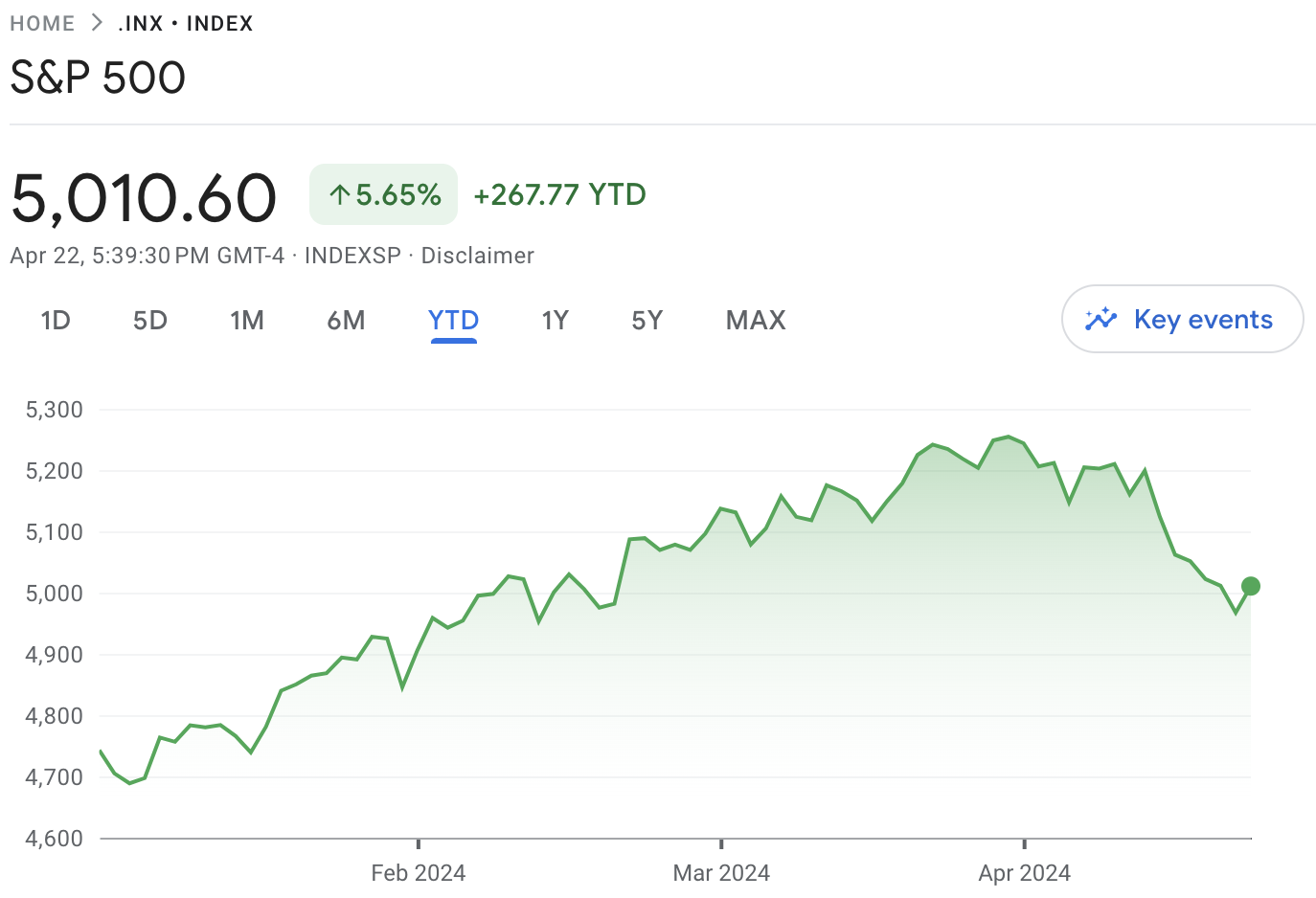

The S&P 500 reacted to the news by retracing sharply from a period of consistent growth that began in late October 2023, posting a decline of more than 5% from its March 28th peak of 5,254.35.

Following the decline, the contrast between the optimistic start to Q1 2024 and Q2 is jarring. While the S&P 500 posted growth of

More pessimism could be on the way. Although the market-implied odds for no cuts to take place at all in 2024 remains low at 11%, confounding inflation figures could see the prospect of a higher-for-longer period of high inflation manifest throughout the year.

According to

At the beginning of the year, forecasts had been suggesting that at least six quarter-percentage point reductions would be likely, and markets had largely priced in lower rates moving into the new year. This makes April’s inflation figures especially worrying. But what’s next for the S&P 500 and Wall Street as a whole?

Keeping Up With Expectations

Wall Street has largely managed to perform well amid historically high interest rates in 2023, so why is the news that rates may stay higher for longer so concerning?

The cause for concern stems from the market’s ability to anticipate events and prices in its expectations many months in advance. The S&P 500’s market rally of more than 25% between late October and late March has been down in no small part to the anticipation that the Fed’s switch to a dovish monetary policy means rate cuts are imminent.

We can see in the index’s rapid 5% drop that these shifting expectations are a key cause for concern among investors, who may be exploring more safe haven strategies while uncertainty creeps back into Wall Street.

Here, the problem stems from the S&P 500’s exceptional form in the wake of Federal Reserve rate cuts. Investors

With the final rate hike arriving on February 1st and the first cut taking place on July 6th of the same year, 1995 became a springboard for growth on the S&P 500, with the index posting 34% growth–its highest annual gain since the 1950s.

As the parallels broke down and CPI data arrived hotter than expected, the timely reality check for the S&P 500 has been particularly tumultuous.

What Will Higher for Longer Look Like?

With interest rate hikes in 2023 coinciding with the generative AI boom, the S&P 500 actually posted a strong annual growth rate of 24%. Should the rate of innovation in this industry continue to facilitate both hype and adoption at an enterprise level, it’s entirely possible that big tech stocks can continue to bring positivity to US markets even during times of high-interest rates.

However, the wider impact of higher-for-longer rates can be varied depending on the impacted stocks and their fundamentals.

While the first interest rate hikes in 2022 saw stocks with high valuations struggle, the 2023 macroeconomic climate forced more investors to look instead at how the bottom line of companies was being impacted by higher rates.

Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management, suggests that this puts smaller companies under the microscope due to issues in funding at higher rates, as opposed to more resilient larger companies with higher liquidity to navigate uncertainty.

Data supports this thesis. While the large-cap stocks populating the S&P 500 Growth Index suffered a 29.41% decline in 2022, the small-cap stocks among the Russell 2000 Index performed better, experiencing smaller losses of 20.44%. These fortunes were reversed in 2023, with the S&P 500 Growth and Russell 2000 posting

This trend is continuing into 2024, and recent disappointment surrounding the expectation of rate cuts is likely to push more investors to look for stocks that offer economic stability, rather than riskier opportunities based on innovation.

With this in mind, the S&P 500 stocks that boast stronger balance sheets and higher cash reserves could become a leading choice on the index, but backtracking rate expectations will likely pave the way for more long-term volatility throughout US markets.

“Given these dynamics, investors may choose to take a balanced approach by diversifying their portfolios to include both safe assets such as gold and riskier assets such as both growth and value stocks,” explained Maxim Manturov, head of investment research at Freedom Finance Europe.

“While cautious optimism may prevail in the stock market, the appeal of gold as a hedge against economic uncertainty remains attractive, from a tactical perspective.”

“Gold's expected upside is emphasized by the speculative potential offered by the NUGT ETF (Direxion Daily Gold Miners Index Bull 2x Shares), presenting an attractive proposition for investors in terms of risk/reward ratio from current levels.”

Diversification Remains Key for Investors

Although we’re experiencing a generative AI boom, the uncertainty of the current economic climate suggests that more diversification should be a priority for investors.

Building exposure to more commodities can be an excellent way of hedging against more disappointment and confounding inflation figures in 2024, but investor optimism can help to drive markets off the back of good news. The record-breaking S&P 500 rally of 1995 will shape sentiment today, and the arrival of any lower-than-expected CPI data could see more optimism flood back into US markets.

While it’s difficult to anticipate Fed rate cuts in 2024, sentiment will continue to shape Wall Street performance throughout the year, and with this in mind, maintaining some levels of exposure can go a long way toward building a sustainable portfolio amid wider market uncertainty.